ACCOUNTS

Double Entry

The Meaning of Double Entry

Explain the meaning of double entry

Businesses need to keep records of their transactions. The process of keeping record is called bookkeeping. The simplest form of bookkeeping is single entry. Every transaction is recorded once. This is unreliable because:

- If an arithmetic mistake is made, it is very difficult to find and correct it

- If a transaction is omitted, it is difficult to find it

Now, a more reliable method of bookkeeping is double entry.

Different Types of Ledger

Explain different types of ledger

Businesses record their accounts in books called ledgers. A ledger is a main book that contains various accounts.

There are three main ledgers:

- The sales ledger

- The purchases ledger

- The general ledger

-The sales ledger: Is the ledger that records the accounts of debtors. The ledger is also known as the debtors’ ledger. A debtor

is a person who owes money to the business, that is a person to whom

the business sold goods on credit. So when the business has a new

customer, it will open an account in the sales ledger for that customer.

is a person who owes money to the business, that is a person to whom

the business sold goods on credit. So when the business has a new

customer, it will open an account in the sales ledger for that customer.

-The purchases ledger: Is the ledger that records the accounts of creditors. This ledger is also known as the creditors’ ledger. A creditor

is a person whom the business owes money, that is a person from whom

the business bought goods on credit. When the business has a new

supplier, it will open an account in the purchases ledger for that

supplier.

is a person whom the business owes money, that is a person from whom

the business bought goods on credit. When the business has a new

supplier, it will open an account in the purchases ledger for that

supplier.

-The general ledger:

Is a ledger that records all accounts other than debtors’ and

creditors’ accountants. Examples of accounts recorded all accounts other

than debtors’ and creditors’ accounts are fixed assets and expense.

Is a ledger that records all accounts other than debtors’ and

creditors’ accountants. Examples of accounts recorded all accounts other

than debtors’ and creditors’ accounts are fixed assets and expense.

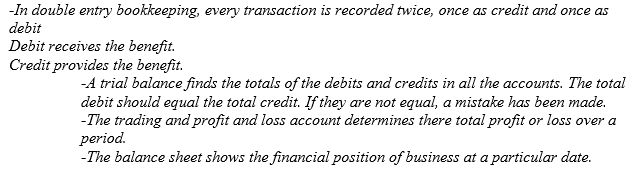

-Double entry: Is a bookkeeping system whereby every transaction is recorded twice in the ledger. It is recorded on the left as debit (DR), and on the right as credit (CR). Every transaction involves the giving and receiving of a benefit.

A Ledger

Construct a ledger

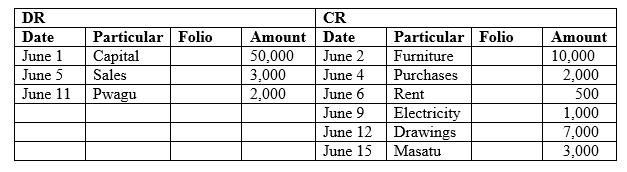

Suppose that a company takes 50,000/- from the bank to pay wages.

- The bank account gives the benefit, and so is credited 50,000/-

- The wages account receives the benefit, and so is debited 50,000/-

Suppose the company buys assets worth 100,000/- from ABC Limited.

- ABC Limited has given the benefit, and so is credited 100,000/-

- The fixed assets account has received the benefit, and so is debited 100,000/-

When transactions are written in a ledger, they are said to be posted to the ledger.

Posting Entries in the Ledger

Post entries in the ledger

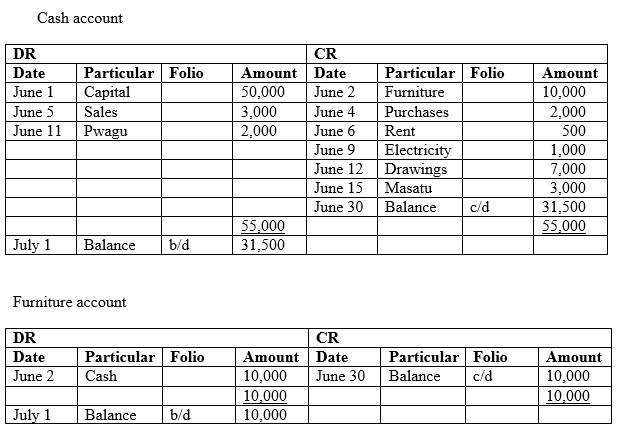

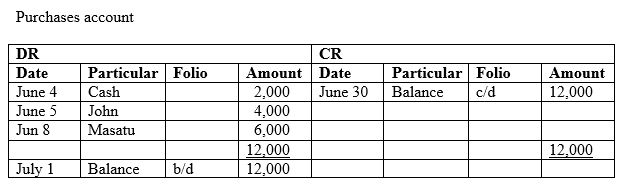

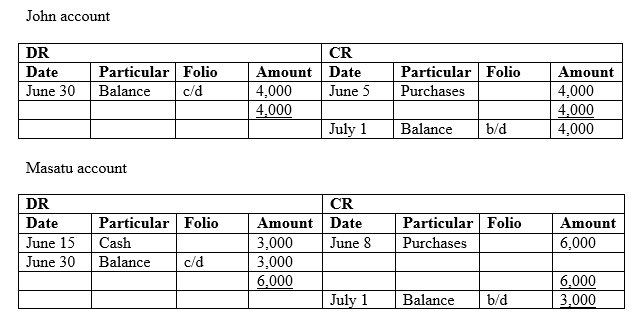

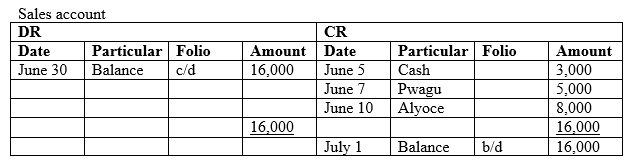

Example 1

The transactions shown in the table below belong to XYZ Traders; Post them to the relevant ledgers.

Solution

In

the first transaction, money is taken from the capital account and

placed cash account. Hence the capital account is credited and he cash

account is debited. In the’ Particular’ column, write the other account

involved in the transaction.

the first transaction, money is taken from the capital account and

placed cash account. Hence the capital account is credited and he cash

account is debited. In the’ Particular’ column, write the other account

involved in the transaction.

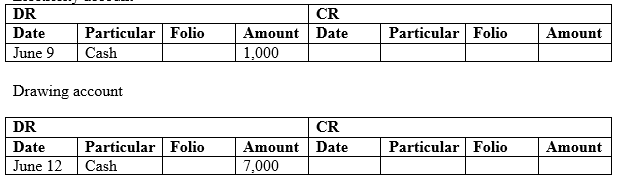

In the second transaction, furniture is bought for cash. So the cash account is credited and the furniture account is debited.

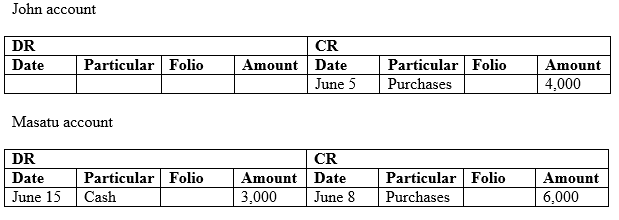

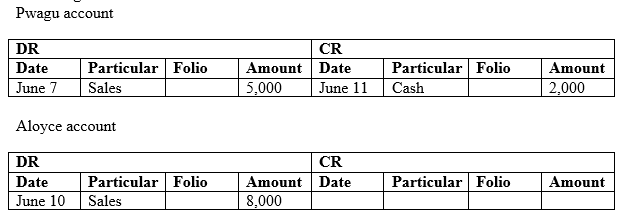

Pwagu

and Aloyce are customers, so they each have accounts in the sales

ledger, John and Masatu are suppliers, so they each have accounts in the

purchases ledger.

and Aloyce are customers, so they each have accounts in the sales

ledger, John and Masatu are suppliers, so they each have accounts in the

purchases ledger.

Other

items are capital, cash, furniture, purchases, sales, rent, electricity

and drawing. They all have accounts in the general ledger.

items are capital, cash, furniture, purchases, sales, rent, electricity

and drawing. They all have accounts in the general ledger.

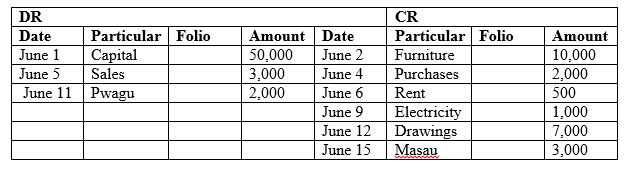

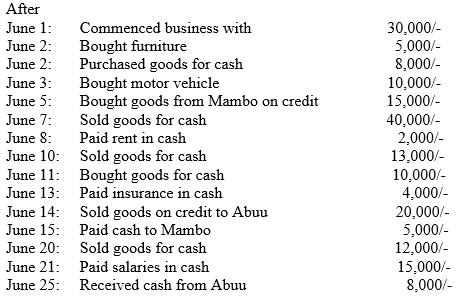

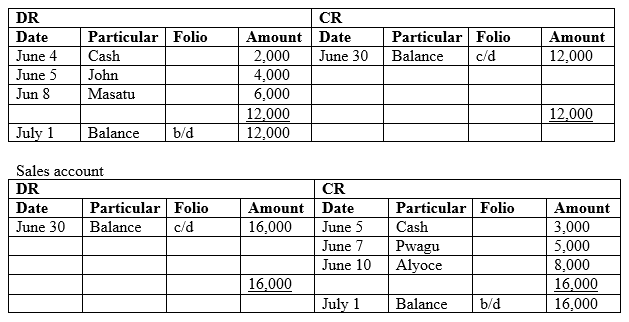

GENERAL LEDGER

Capital account

Cash account

Furniture account

Purchases account

Electricity account

PURCHASES LEDGER

Sales ledger

Note: Check that for each transaction there are two equal entries, one for debit and one for credit, for instance:

June 11: Received cash from Pwagu, 2,000

-Pwagu’s account is credited 2,000

-The cash account is debited 2,000

This is what is meant by double entry.

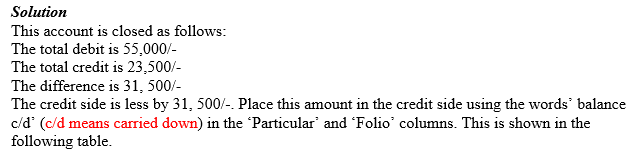

Closing the Simple Accounts

Close the simple accounts

Closing

the accounts is the process of balancing the accounts. This involves

determining the totals of the debits and credits, and finding the

difference between the two sides. The difference is the balancing figure, which is placed in the side that is less. This makes the two sides equal.

the accounts is the process of balancing the accounts. This involves

determining the totals of the debits and credits, and finding the

difference between the two sides. The difference is the balancing figure, which is placed in the side that is less. This makes the two sides equal.

Example 2

Consider the following account from Example 1. Close this account.

Cash account

Cash account:

The

balance c/d shows the amount that stands on the account on the closing

date. It appears as balance b/d (b/d means brought down) on the opening

date of the next trading period, on the other side of the ledger.

balance c/d shows the amount that stands on the account on the closing

date. It appears as balance b/d (b/d means brought down) on the opening

date of the next trading period, on the other side of the ledger.

Exercise 1

1. What is a ledger? Give an explanation of three ledgers you know, with an example of accounts kept in each ledger.

2. For each of the following transactions, name the ledger it would be posted to, and whether this would be as credit or debit.

- a lorry bought for cash

- goods sold to Mr. Sabaya for cash

Trial Balance

The Concept of Trial Balance

Explain the concept of trial balance

Trial balance

is a statement which shows the balances of accounts extracted from the

ledger. At the end of each trading period, the accounts in the ledger

are closed, that is the balance of each account is determined. These

balances are then shown in the trial balance.

is a statement which shows the balances of accounts extracted from the

ledger. At the end of each trading period, the accounts in the ledger

are closed, that is the balance of each account is determined. These

balances are then shown in the trial balance.

Below is the format of a trial balance.

TRIAL BALANCE as at 30 June 2005

Accounts with debit balances are posted in the DR column and those with credit balances in the CR column.

Functions of trial balance

The trial balance serves the following two major roles:

-It

checks the arithmetical accuracy of the ledger. The double entry system

requires posting equal amounts to debits and credits. Therefore the

trial balance is expected to balance if the arithmetic was correct. If

there is a difference in the totals of the debit and credit columns of

the trial balance, then some errors were made.

checks the arithmetical accuracy of the ledger. The double entry system

requires posting equal amounts to debits and credits. Therefore the

trial balance is expected to balance if the arithmetic was correct. If

there is a difference in the totals of the debit and credit columns of

the trial balance, then some errors were made.

-It

simplifies the preparation of the final accounts. The trial balance

contains all the accounts extracted from the ledgers. This makes it easy

to post the accounts to the final accounts.

simplifies the preparation of the final accounts. The trial balance

contains all the accounts extracted from the ledgers. This makes it easy

to post the accounts to the final accounts.

Construction of Trial Balance

Construct trial balance

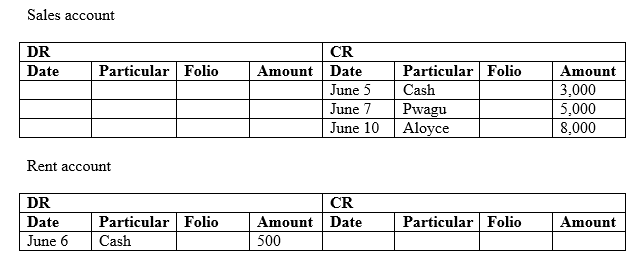

Look again at Example 1 of XYZ Traders. The accounts, after being closed, appear as follows:

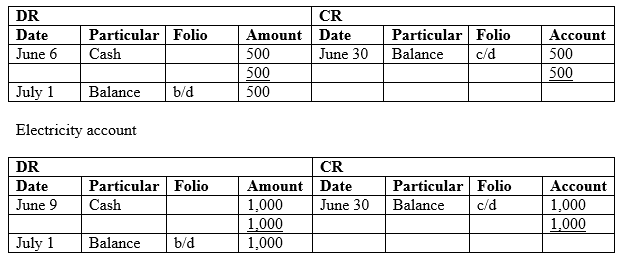

Purchases account

Rent account

And other accounts closing.

NB. The balance b/d determines whether the account has a debit or credit balance.

Example 3

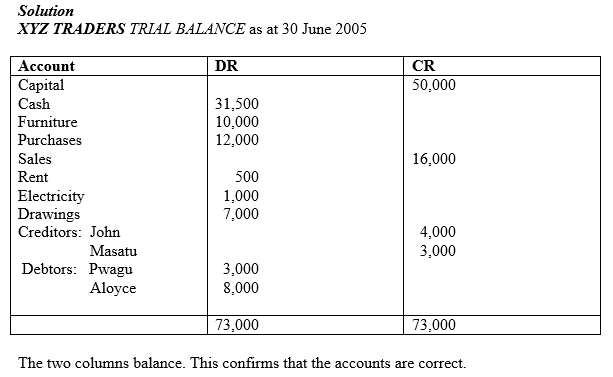

Construct the trial balance for XYZ Traders of Example 1.

Exercise 2

1. Why is trial balance referred to as statement of arithmetical accuracy?

2. Trial balance is statement and not part of double entry. explain why?

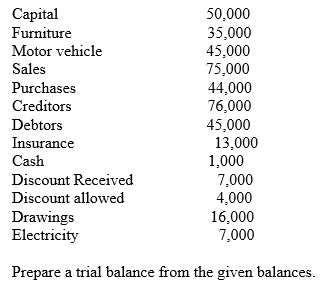

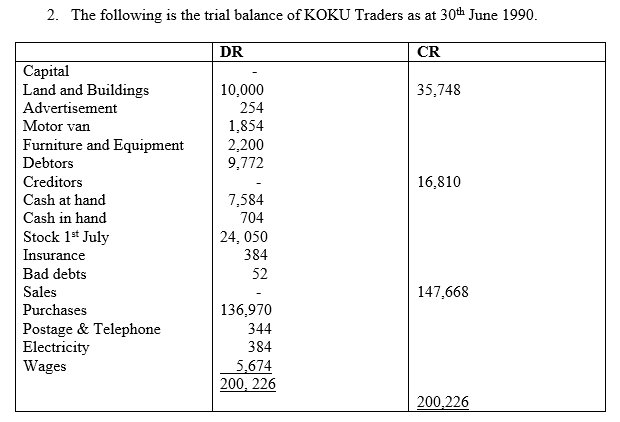

3. The following balances were extracted from the ledgers of Doka traders on 30 June 2005.

Debit Balances and Credit Balances

Post debit balances and credit balances

DEBIT BALANCES:

CREDIT BALANCES:

Checking the Balances

Check the balances

Activity 1

Check the balances

Trading Profit and Loss

Gross Profit/Loss using Trading Account

Ascertain gross profit/loss using trading account

The

trading and profit and loss A/C is an account that is composed of two

accounts, the trading A/C, and the profit and loss A/C.

trading and profit and loss A/C is an account that is composed of two

accounts, the trading A/C, and the profit and loss A/C.

The trading A/C is used to determine the gross profit of the goods sold:

Gross profit = sales – cost of goods sold

The profit and loss account (A/C) is the part of the account that determines the net profit loss:

Net profit = gross profit – expenses

Net loss = expenses – gross profit

-In

the profit and loss A/C, the gross profit and other revenues are

credited to the account while the operating expenses are debited.

the profit and loss A/C, the gross profit and other revenues are

credited to the account while the operating expenses are debited.

-We have net profit if the credit is greater than the debit and net loss if the debit is greater than the credit.

Example 4

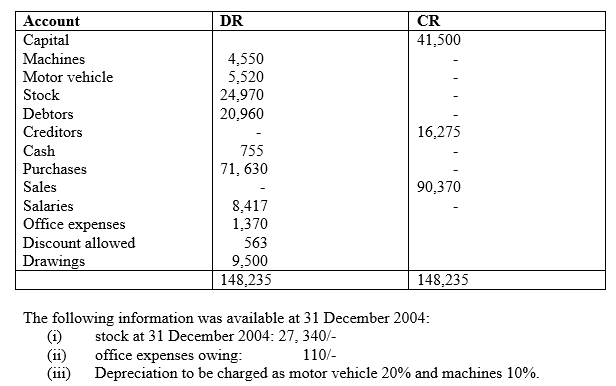

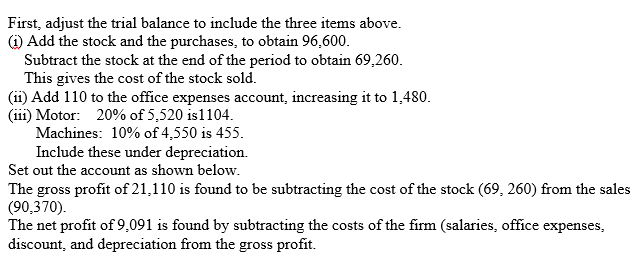

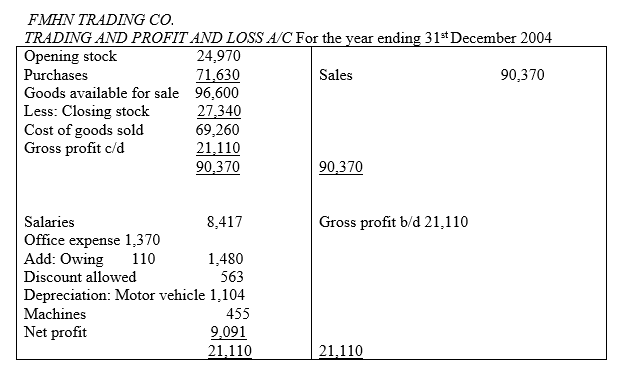

The

following is the trial balance of FMHN Trading Co. as at 31 December

2004. Prepare the trading and profit and loss accounts for the year

2004.

following is the trial balance of FMHN Trading Co. as at 31 December

2004. Prepare the trading and profit and loss accounts for the year

2004.

FMHN TRADING CO.

TRIAL BALANCE as at 31 December 2004

Solution

Net Profit/Loss Account

Ascertain net profit/loss account

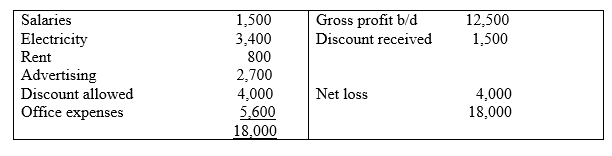

When net loss is recorded, the profit and loss A/C appears as shown in the following example.

PROFIT AND LOSS A/C

For the year ending ……………………

Exercise 3

1. Explain the function of trading A/C.

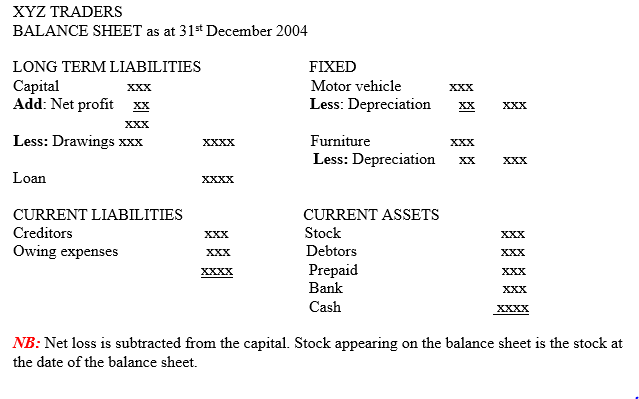

A Balance Sheet

Construct a balance sheet

A balance sheet is a statement which shows the financial position of a business at a particular date.

It shows the assets on one side and liabilities on the other.

Assets are divided into two: fixed assets and current assets.

-Fixed assets

are possessions of the business that assist the business in its

operations, and benefit the business for more than one accounting

period.

are possessions of the business that assist the business in its

operations, and benefit the business for more than one accounting

period.

-Current assets are assets of the business used in generating income during the accounting period.

Liabilities are also grouped into two: long term liabilities, which are payable in more than one accounting period and current liabilities, which are payable within the accounting period.

The following is the format of balance sheet showing the common items of the balance sheet.

Posting Entries in Balance Sheets

Post entries in balance sheets

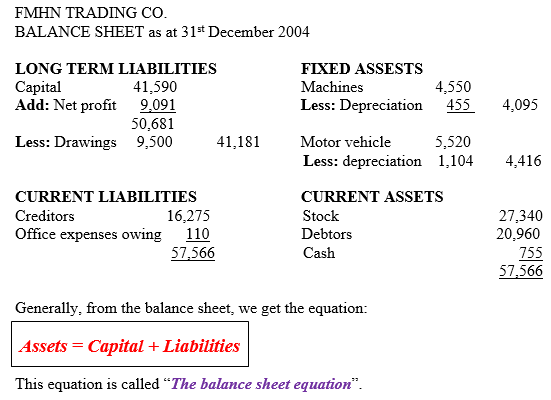

Example 5

Considering FMHN Trading Co. from above example, the balance sheet will be as

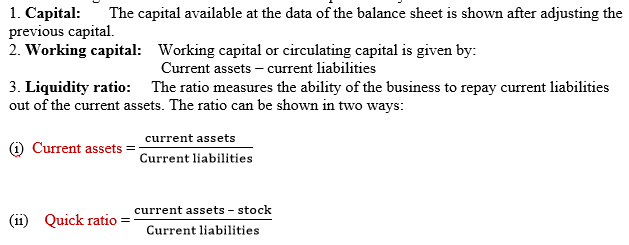

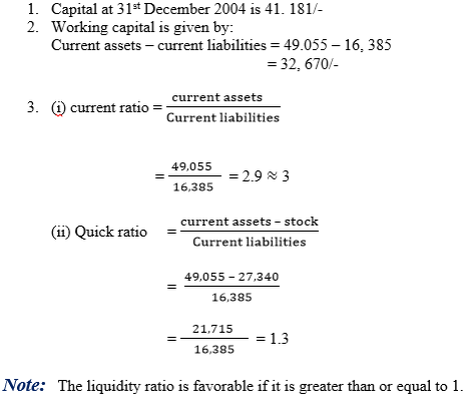

Interpreting Information from the Balance Sheet

Interpret information from the balance sheet

From

the balance sheet, useful information concerning the business can be

extracted. The interpretation then depends on the use of the

information.

the balance sheet, useful information concerning the business can be

extracted. The interpretation then depends on the use of the

information.

The following are some of the useful information provided by the balance sheet.

The

quick ratio measures the ability of the business to pay current

liabilities out of current assets excluding stock which is considered

less liquid.

quick ratio measures the ability of the business to pay current

liabilities out of current assets excluding stock which is considered

less liquid.

From the balance sheet of FMHN Trading Co. we can find the following.

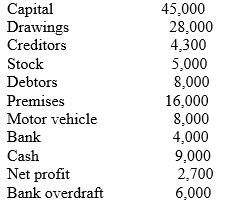

Exercise 4

1. Prepare the balance sheet for the balances given in the table below.

2. From the balance sheet constructed in question 2, determine the following.

- Working capital

- Quick ratio

- Current ratio

Summary

Exercise 5

1. Explainan advantage of double entry bookkeeping over single entry bookkeeping.

2. Givethree accounts that would be kept in the general ledger.

3. Define the quick liquidity ratio.

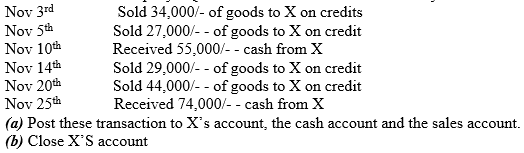

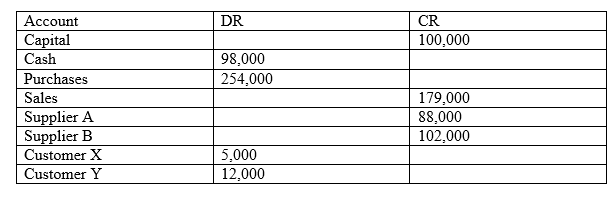

4. Xis acustomer of company PQR. Below are the transaction made by X over a month.

5. The following table shows the closing balances of company PQR of question 4.

6.

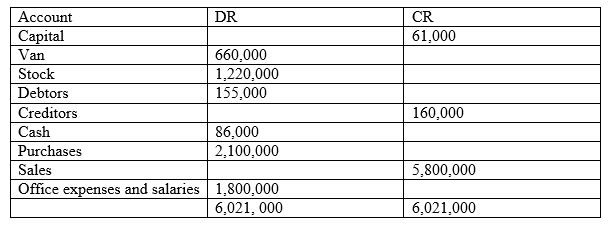

Below is a trial balance for Nyati Ltd. The closing stock was 1,

750,000/-, and the van was depreciated at 25%. Set up the trading and

profit and loss account.

Below is a trial balance for Nyati Ltd. The closing stock was 1,

750,000/-, and the van was depreciated at 25%. Set up the trading and

profit and loss account.

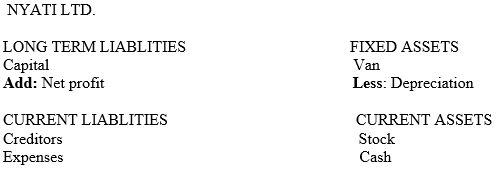

7. Complete the balance sheet below for Nyati Ltd. of question 6.

8. Use the balance sheet constructed in question 7 to find the following.

- capital

- working capital

- current liquidity

- quick liquidity rate